How Does NZ Super Work For Your Retirement?

One of the most important questions I hear clients ask is: What is the role of New Zealand Super for my retirement?

Today we answer that question.

1. What Is NZ Super

NZ Super is taxable income paid by the Ministry of Social Development from age 65 onwards.

You receive it whether you have:

$0 invested

$500,000 invested

$5,000,000 invested

There is no reduction based on your portfolio size.

The one thing to be aware of is this:

If you continue working while receiving NZ Super, the Super is treated as secondary income for tax purposes. That means you’ll likely notice higher PAYE deductions applied to it.

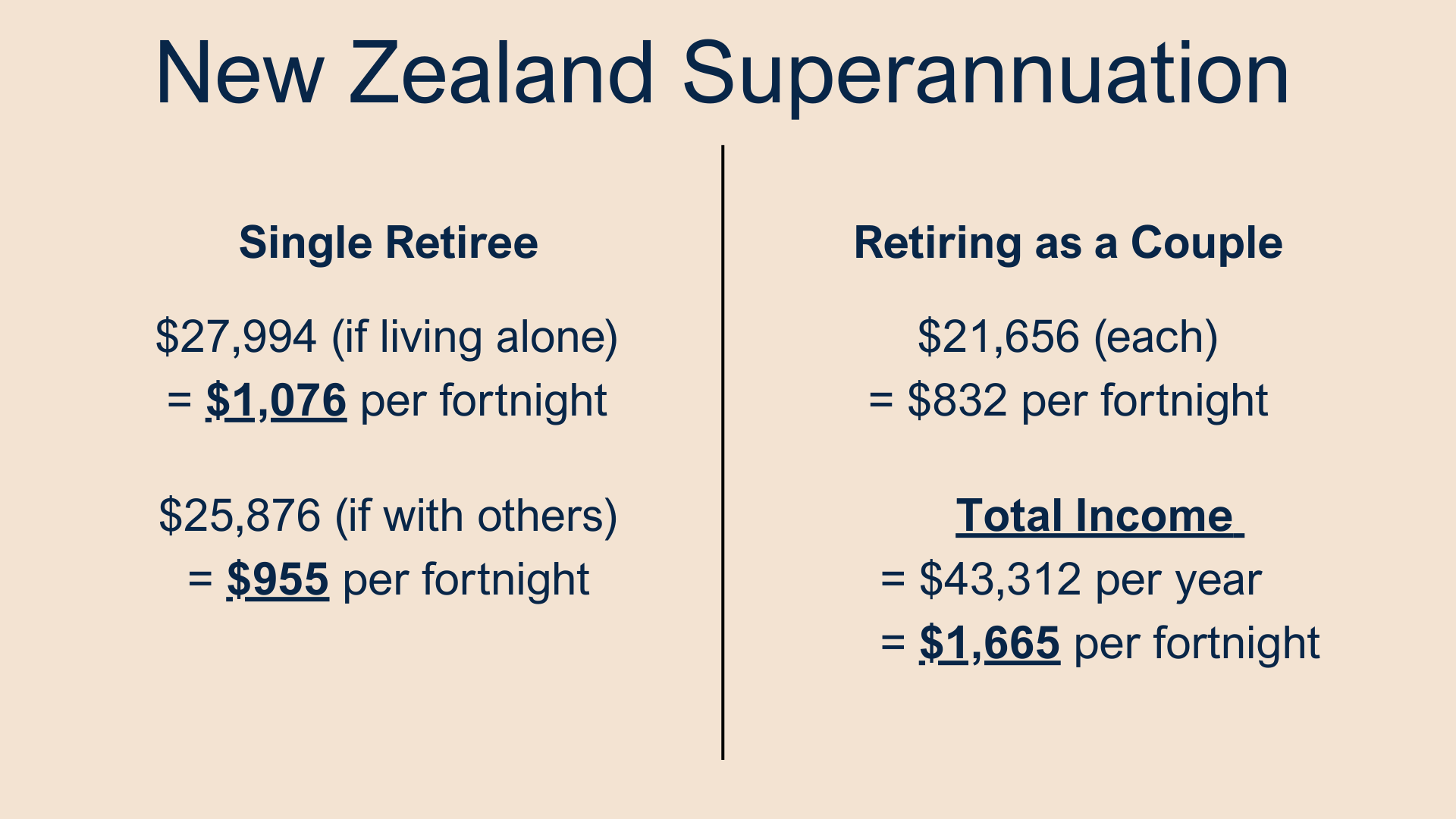

As of the 2025-26 tax year (these rise each year to account for wage inflation in April), current entitlements are as follows:

2. NZ Super Is Your “Base Income Layer”

In developing a retirement plan, we should think in layers for income.

Layer 1: NZ Super

Layer 2: Your diversified investment portfolio

Layer 3: Other incomes - rental income, part time work, business income

NZ Super forms the foundation.

If you are a couple receiving around $43,000 per year, that is the equivalent of having roughly $1,000,000 invested for you. Therefore, before making any drawings from your portfolio the government is effectively covering a meaningful portion of your essential spending.

For many Auckland retirees with mortgage-free homes, NZ Super alone covers rates, insurance, utilities, basic groceries, and a modest lifestyle.

Your portfolio then funds lifestyle flexibility - travel, gifting, and experiences.

3. What NZ Super Does To Your Required Capital

This is where planning becomes powerful.

Let’s say a couple wants $90,000 per year after tax to live comfortably in Auckland.

If NZ Super provides $43,000 gross, their portfolio may only need to fund the remaining approx. $47,000 per year.

That can dramatically lower:

Required investment portfolio size

Sequence of returns risk

Emotional stress during market volatility

4. It Is Unlikely To Change Your Portfolio Risk Settings

Some people look at NZ Super and assume that means they should take high levels of investment risk. Others assume it means they do not need to invest at all.

Neither is entirely accurate.

In practice, the most appropriate amount of risk for your investment portfolio (e.g. Conservative, Balanced, Growth or High Growth) should be determined by the two main risk capacities for retirement:

The risk you are comfortable taking as aligned to a psychometric investment risk assessment

The risk you need to take with your capital to support your retirement for the duration

5. Importantly, Residency Matters

To qualify, you must meet residency requirements. This is currently 10 years in New Zealand since age 20, including 5 years after age 50, with changes gradually extending this.

If you have lived overseas, things can become more complex depending on your eligibility for overseas social security and associated intercountry agreements.

For high net worth or internationally mobile clients, this is an area worth checking with an expert.

Final Thought

New Zealand is one of the few countries in the world that provides a universal, wage inflation-indexed pension with no asset testing.

The opportunity is to use your diversified investment portfolio to build on that foundation, creating a capital base that supports the parts of life that bring meaning and enjoyment including regular travel, dining out, and spending on the interests that matter to you.