What are Wealth Management fees in Auckland?

If you are considering wealth management or investment advice, you likely want to know two things before anything else: what is this going to cost you, and what value am I likely to receive?

This article answers both and covers how the industry works in enough detail that you can make a useful comparison between firms.

What Do Wealth Management Fees Actually Cost?

The most common fee structure in New Zealand wealth management is a percentage of the assets being managed, charged annually. This is called an assets under management (AUM) fee.

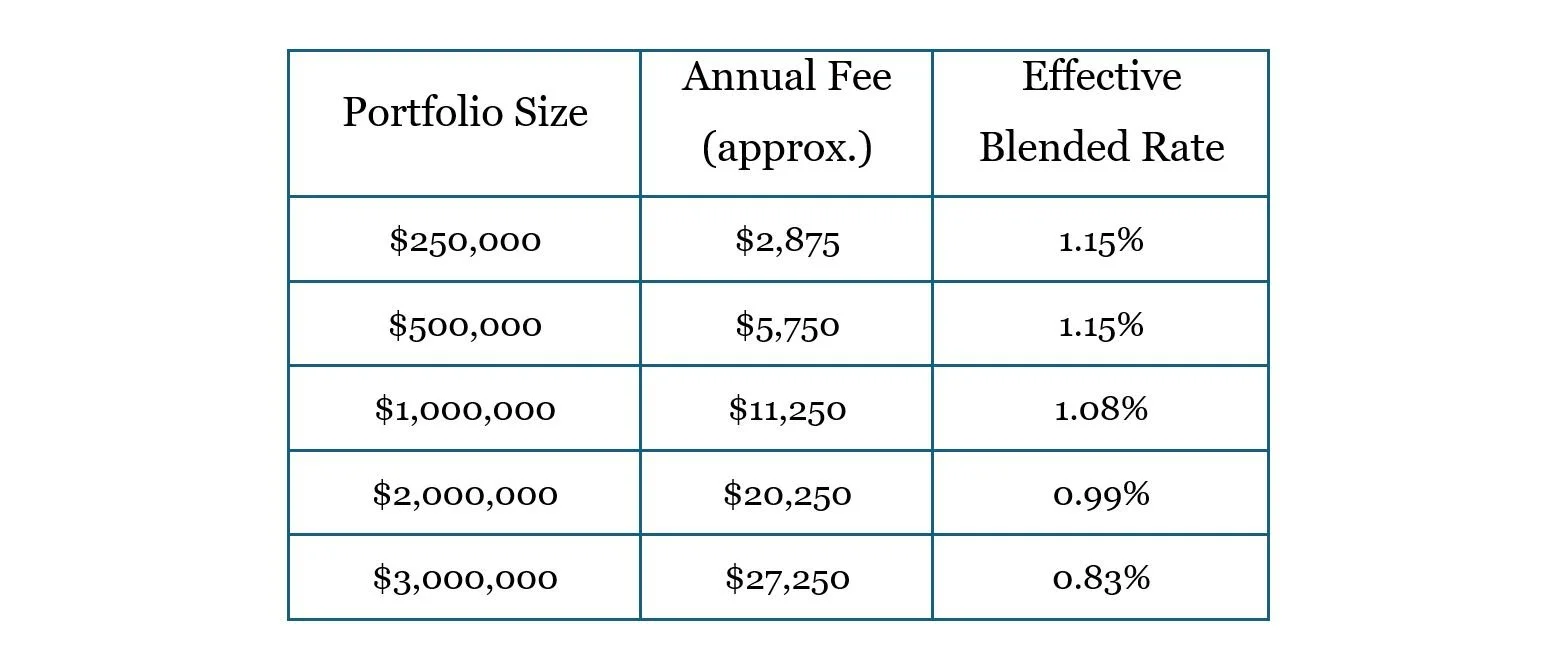

In Auckland, that percentage typically sits between 1% and 1.2% per annum at entry level, stepping down progressively as your balance increases.

To make it clear, here is how the blended annual fee works out under a typical tiered structure (1.15% on the first $500k, 1.00% on the next $500k, 0.90% on the next $1m, 0.50% above $2m).

The blended annual fee typically follows a tiered structure similar to the following:

These fees are usually deducted from the portfolio automatically each month. For investment sums substantially higher than this, I’ve seen the blended fee come down as low as 0.40% per year, however this is usually by negotiation with your Wealth Manager.

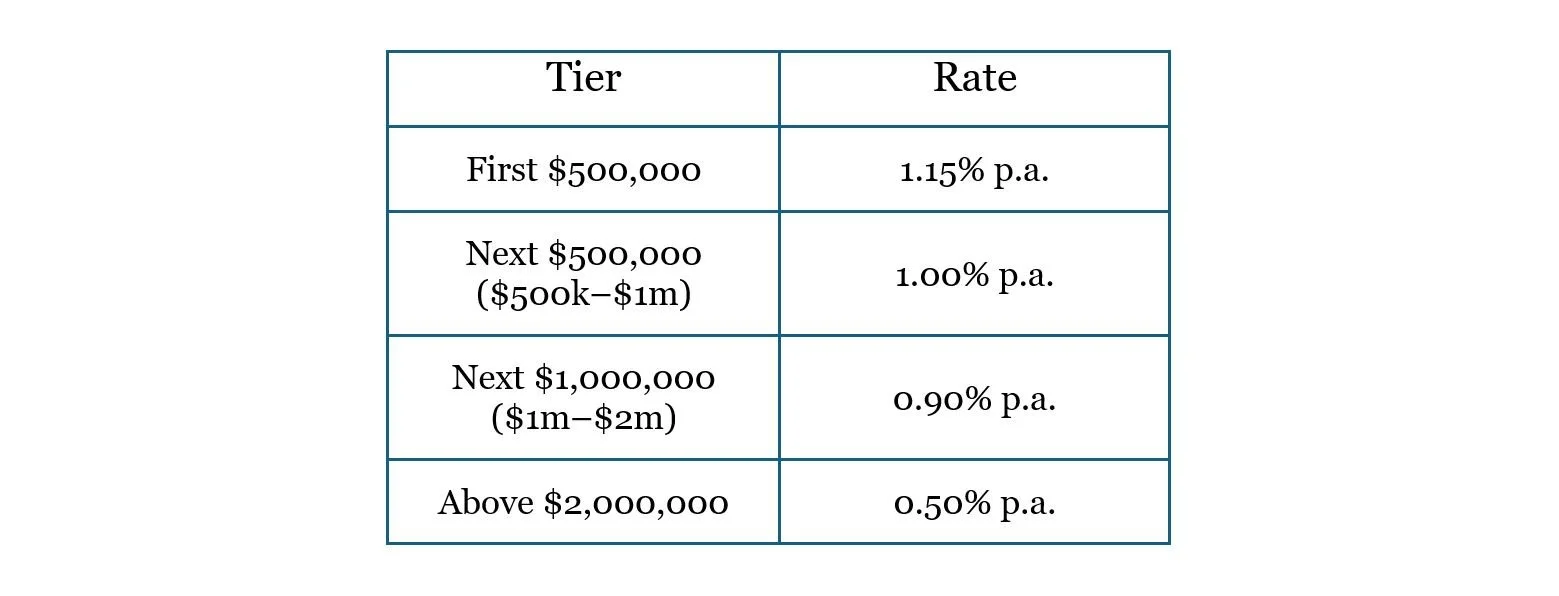

How the Tiered Fee Structure Works

Most wealth management firms apply a progressive fee schedule, where the percentage rate reduces at higher asset levels. This works similarly to a progressive tax: each tier of your portfolio is charged at a different rate, and the rates step down as the balance increases.

A typical fee schedule will look like this:

Under this structure, if you had $1,500,000, you would not simply pay 0.90% on the whole amount. You would pay 1.15% on the first $500,000 ($5,750), 1.00% on the next $500,000 ($5,000), and 0.90% on the remaining $500,000 ($4,500), for a total annual fee of $15,250 - an effective blended rate of around 1.02%

This means larger portfolios attract a lower percentage overall, but the dollar amount continues to grow with your balance. Firms use different tiers, breakpoints and rates, so it is worth asking any prospective adviser for a fee illustration based on your actual situation.

What These Fees Don't Include

The adviser fee is not the only cost. You also pay for:

Platform fees: the cost of the investment administration platform, often between 0.10% and 0.25% p.a.

Underlying fund costs: the management fees charged by the funds or managed portfolios within your account, ranging from around 0.10% to 0.40% p.a. for index funds and 0.60% to 1.00% p.a. or more for actively managed funds

These costs are separate from the adviser fee and are often disclosed in fund documents rather than the adviser's fee schedule. Adding all layers together, your total investment costs may sit somewhere between 1.4% and 2.5% per annum depending on the firm, the investment approach, and the fee tier.

Why Pay For Wealth Management?

The existence of low-cost index funds is not a secret. You can build a broadly diversified global portfolio through a handful of index funds for somewhere between 0.1% and 0.5% per annum total — significantly lower than the cost of a managed wealth advisory relationship.

So why do some people pay $5,000, $10,000, or $20,000 per year to a wealth manager?

For Mass Affluent and High Net Worth Investors, Mistakes Are Expensive

When you are managing $500,000 or more, a 10% loss is equal to $50,000. At $2,000,000, the same market move is $200,000. The stakes of poor decisions — whether that is poor investment structuring, panic-selling, or poorly structuring for tax — scale directly with your portfolio size.

A good wealth manager carries the experience of having worked with dozens of clients across every kind of market and life event. They have seen people in similar positions make the same mistakes: selling in a downturn, concentrating too heavily in a single asset or industry, or mistiming a reinvestment after a business sale. By working with a wealth manager, you effectively inherit that accumulated wisdom — the experience of many lifetimes in practice, not just your own.

Your Financial Life Has Genuine Complexity

A straightforward accumulation investor with a single portfolio and no other complexity probably doesn't need a full-service wealth manager. But if you are approaching retirement, have sold or are selling a business, hold assets across multiple entities or trusts, have an estate that needs structuring, or are navigating a significant inheritance, your financial life likely has real complexity - and the interactions between those moving parts need to be addressed.

A strong wealth manager acts as a connector. They are not just managing your portfolio; they are identifying when you need a specialist, whether that is a tax lawyer, an estate solicitor, an accountant with specific expertise, or another professional. They understand enough about law and tax to recognise when a problem is about to arise, and to bring in the right person before it does rather than after. For clients with meaningful complexity, this coordination function alone can justify the fee several times over.

You Want Somebody You Can Call

One of the most consistent things clients describe valuing in an advisory relationship is having someone to call when a major life change is on the horizon - a business sale, a health scare, an unexpected inheritance, a question about whether to sell an investment property - and receiving a clear, calm, and informed response with plan to move forward.

This may feel valuable for you as well.

The Context of Portfolio Growth Against Cost

Over the long term, a diversified balanced portfolio has historically returned around 7% to 8% per year. Against that backdrop, an advice fee of around 1% represents a meaningful but manageable share of expected long-term returns, particularly when weighed against the cost of the mistakes it may help you avoid. For an investor moving out of term deposits into a diversified portfolio for the first time, a wealth manager who keeps you invested through volatility and positioned for long-term growth can more than justify the fee.

Other Fee Structures

AUM-based fees dominate the New Zealand market, but other models exist.

Flat fees and retainers: Some advisers, particularly those focused on financial planning rather than portfolio management, charge a fixed annual fee independent of portfolio size. Ongoing retainers for planning-focused relationships might run $5,000 to $15,000 per year. A comprehensive one-off financial plan might cost $2,000 to $8,000 as a project fee. Some firms are also merging AUM fees with retainers, opting for a lower AUM fee (often around 0.5% per year) and charging a fixed retainer on top.

Hourly advice: Uncommon but available. Rates typically range from $200 to $400 per hour. Useful for clients who need specific advice without an ongoing relationship.

What "Wealth Management" Actually Covers

The phrase is used loosely across the industry, and different firms mean different things by it.

At its broadest, wealth management can include investment management, retirement and cashflow planning, KiwiSaver advice, insurance structuring, estate planning, trust and entity structuring, tax coordination with accountants, business succession planning and behavioural coaching.

Most firms won't deliver all of these with equal depth. Some relationships are primarily investment management with lighter planning involvement. Others are planning-led, where the investment portfolio is one component of a broader strategic conversation. A smaller number of firms focus on high-complexity private wealth, covering trusts, succession, estate structuring, and multi-generational wealth transfer and coordination.

Understanding which category a firm actually operates in is one of the more useful things you can do before signing an engagement agreement.

Not All 1% Fees Are Equal

Two firms here in Auckland charging around 1% on a $1,000,000 portfolio are billing similar amounts. However, the service experience behind that fee can look completely different.

Differences may include:

Meeting frequency: one review per year versus quarterly contact

Responsiveness: days-long turnaround versus same-day replies

Planning depth: investment portfolio only versus full financial planning and estate coordination

Proactive communication: waiting for you to call versus reaching out before major decisions

Breadth of expertise: investments only versus trusts, tax, estate, insurance

Implementation support: telling you what to do versus handling the paperwork with you

Market communication: silence during downturns versus clear, calm updates

The challenge is that vastly different service experiences are often marketed under very similar language.

"Personalised service."

"Long-term relationships."

"Holistic advice."

These phrases appear on almost every firm's website regardless of what you may receive.

Questions Worth Asking Before You Engage

On scope and service:

What is actually included in the annual fee? Is this primarily investment management, or does it include broader financial planning?

Who manages the investments? Is it the adviser directly, or a centralised investment team?

How often will I hear from you proactively, outside of scheduled reviews?

What due diligence do you undertake on the funds you use?

On fees and total cost:

Can you provide a fee illustration based on my specific portfolio size?

What are the underlying platform and fund costs, on top of the adviser fee?

How does the fee change as my portfolio grows or shrinks?

On the relationship:

What does a review meeting actually cover? Is it a portfolio update, or a broader financial conversation?

What happens when markets fall significantly? What should I expect from you?

Do you coordinate with my accountant or lawyer when needed? Follow up if yes, what work have you done in the past with an accountant or lawyer?

This article is general in nature and does not constitute personalised financial advice. For advice specific to your circumstances, consult a licensed financial adviser.